A reader from down under asks:

You guys have been talking a lot about US economic exceptionalism in recent years with the caveat that houses are too expensive. Fair enough. But check out housing prices in Australia where I live. It’s madness!

People have been saying it’s a bubble for years while prices just keep going higher. I don’t really have a question. Just wanted to point out that prices in the states look tame by comparison. Cheers.

I am in complete agreement with my Australian friend here.

While it seems like the U.S. housing market is completely broken and prices are out of reach for millions of Americans, the situation is much worse in other countries.

Especially Australia.

The median price for an existing home in the United States is around $410,000. In Australia it’s more than $800,000. In Syndey, the median price of a home is well over $1 million.

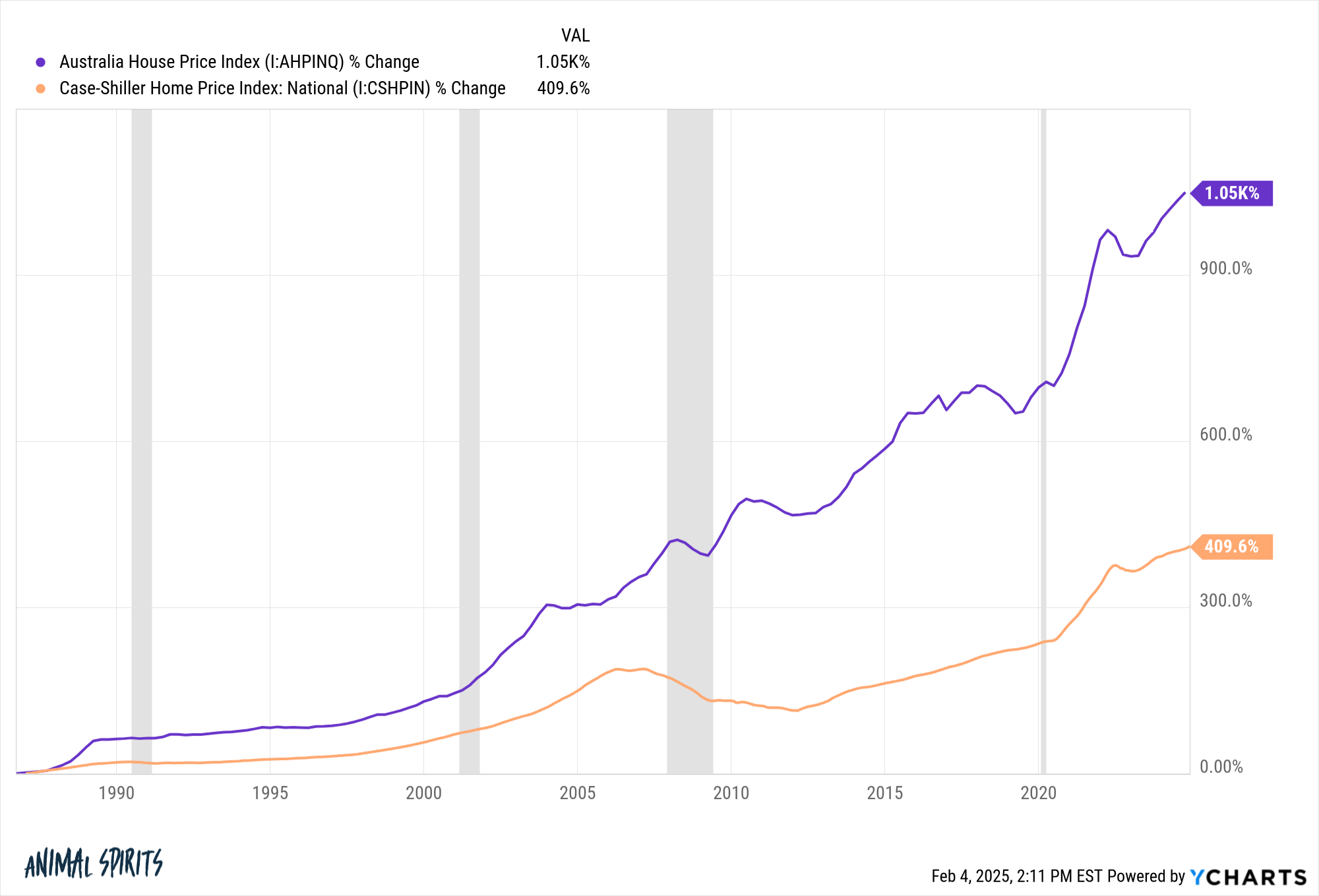

Homeowners in the U.S. have experienced incredible gains over the past 30-40 years but we’ve got nothing on Australia:

Since the late-1980s, housing prices down under have more than doubled up our returns on homeownership.

It’s also import to put these price gains into context in terms of affordability. I like to do this by comparing price gains to wage gains.

These charts show housing price growth versus the growth in disposable income for both the United States and Australia going back to 1975:

I put these time series on the same scale to show just how out of whack this relationship is in Australia. In the U.S., housing prices and disposable incomes have grown roughly in lockstep with one another.

Not so in Australia where the chart looks like an alligator opening wide and showing off its teeth.

Some people prefer using inflation-adjusted data when making comparisons across borders:

The real data paints a similar picture.

Torsten Slok has a great chart that compares household debt to disposable income in the U.S., Canada and Australia:

Canada and Australia have seen debt-to-income ratios rise for years now while U.S. households have been repairing their balance sheets ever since the Great Financial Crisis. Higher housing prices are obviously the main culprit here

Mortgage debt makes up 70% of household debt in the U.S. I don’t have the exact figures for Australian households but I’m guessing it’s a similar profile.

But it’s not just higher housing costs that are hurting Australian household balance sheets. Higher interest rates in recent years have hurt most homeowners because of how their mortgage market is structured.

The following chart shows debt to income by country plotted against the usage of variable rate mortgages:

You can see Australia has one of the highest shares of variable-rate mortgages.

As far as I can tell you’re able to lock in your rate for around 5 years and then it resets. This was a wonderful set-up when rates were falling, but now that we’re in a higher interest rate world, it is more expensive for current and new homeowners alike.

U.S. homeowners were able to lock in 3% mortgage rates during the pandemic to shield themselves from a rising rate environment. That’s not the case in many other countries because they don’t utilize 30 year fixed rate mortgages like we do.

Does looking at someone else’s situation make those struggling to buy a home in America feel any better about their own situation?

Of course not!

But it’s worth pointing out that as bad as the housing market seems right now in the U.S. from an affordability perspective it could always be worse. It is worse in plenty of other countries.

And it’s possible we could see affordability get even worse here if we don’t make it easier to build more homes to fix our housing shortage.

We covered this question on the latest episode of Ask the Compound:

[embed]https://www.youtube.com/watch?v=k71f2WcHNB4[/embed]

Bill Sweet joined me on the show this week to discuss questions about the tax benefits of owning rental properties, the tax implications of an inheritance, retirement planning for military service members and how tariffs work.

Further Reading:

The U.S.

Housing Market vs. The Canadian Housing Market

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services.

Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated. Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails.

Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures here.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by finopulse.

Publisher: Source link